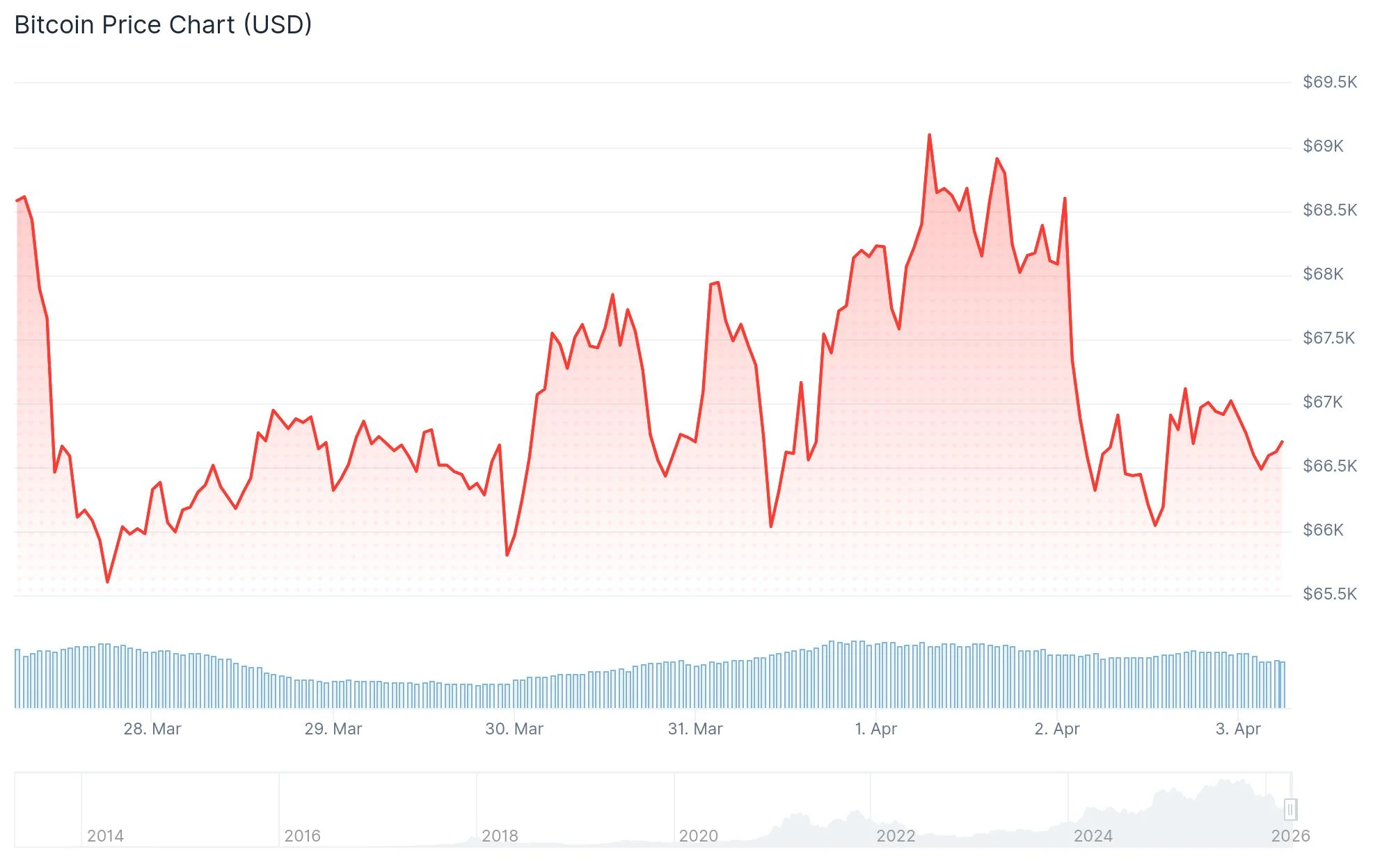

Dips to $66,600 Amid Easter Weekend Trading Lull While Equities Break Five-Week Decline")

Key Highlights

- Bitcoin hovers near $66,600 as Good Friday brings trading pauses across CME futures and spot ETF platforms

- Net Bitcoin demand registers -63,000 BTC even as ETF inflows and institutional buying reach multi-month peaks

- Whale-sized wallets holding 1,000–10,000 BTC shift to distribution mode, declining approximately 188,000 BTC from cycle highs

- Major equity indices break a five-week decline, posting modest weekly gains despite choppy Thursday trading

- WTI crude oil posts unprecedented $11.42 jump to $111.54, marking the steepest single-session gain since 1983

The leading cryptocurrency enters the Easter holiday period facing headwinds, even as traditional equity markets managed to halt a prolonged downturn with marginal weekly advances.

Bitcoin was changing hands around $66,600 Thursday afternoon as Good Friday trading halts shuttered CME derivatives and ETF platforms. This temporary pause eliminates two critical demand channels precisely when buying activity has already weakened considerably.

According to CryptoQuant analytics, the 30-day apparent demand metric currently registers approximately -63,000 BTC. This negative reading persists despite spot Bitcoin ETF acquisitions totaling roughly 50,000 BTC throughout the past month—the strongest accumulation level observed since October 2025.

Strategy, the prominent corporate Bitcoin accumulator, contributed approximately 44,000 BTC during this same timeframe. However, distribution from other market participants proved substantial enough to offset these combined institutional purchases.

Whale Wallets Shift to Distribution Phase

The most pronounced selling pressure originates from substantial holders. Wallet addresses containing between 1,000 and 10,000 BTC have transitioned into net distribution mode. Their annual balance modification has deteriorated to approximately -188,000 BTC, reversing from a positive 200,000 BTC recorded at the 2024 market cycle zenith.

Medium-tier holders have likewise decelerated their accumulation patterns. The Coinbase Premium indicator has maintained negative territory, traditionally signaling diminished appetite from U.S.-based spot market participants.

Singapore-headquartered liquidity provider Enflux informed CoinDesk that Bitcoin’s support level remains partially dependent on Federal Reserve monetary policy expectations. This foundation currently faces significant examination.

The ISM manufacturing prices-paid component surged to 78.3 during March, representing its most elevated reading since June 2022. Such inflationary pressure diminishes the probability of imminent rate reductions, consequently undermining Bitcoin’s macro-supported valuation floor.

ETF movement data already demonstrates this transition. The March 24 week recorded $296 million in aggregate ETF withdrawals. Early April inflow activity has remained subdued.

CryptoQuant analysts identified a resistance corridor spanning $71,500 to $81,200 for any prospective recovery movement. The subsequent crucial economic release arrives with U.S. core PCE inflation figures scheduled for April 9.

Equity and Energy Markets

U.S. stock indices concluded the week with gains notwithstanding Thursday’s turbulent session. The Dow Jones Industrial Average declined 61 points during the final trading day, yet all three primary benchmarks registered positive weekly performance, terminating a five-week consecutive decline.

The trading session was characterized by extraordinary volatility in energy markets. West Texas Intermediate crude settled at $111.54 per barrel, representing an 11% single-day advance. The absolute dollar appreciation of $11.42 constitutes the largest one-day WTI movement in historical data extending back to 1983.

This dramatic surge followed President Trump’s public remarks addressing ongoing tensions with Iran, which provided no substantive progress toward resolving the Strait of Hormuz closure situation.

J.P. Morgan strategist Fabio Bassi projected that crude prices will likely maintain elevated levels throughout the second quarter. He positioned near-term risk within the $120–$130 per barrel band, with scenarios exceeding $150 becoming feasible should Strait disruptions persist into mid-May.

Market participants will simultaneously monitor the March nonfarm payrolls release, scheduled for Friday publication despite equity market closures. Economic forecasters anticipate employment growth to rebound following February’s weather- and labor-strike-impacted figures.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants