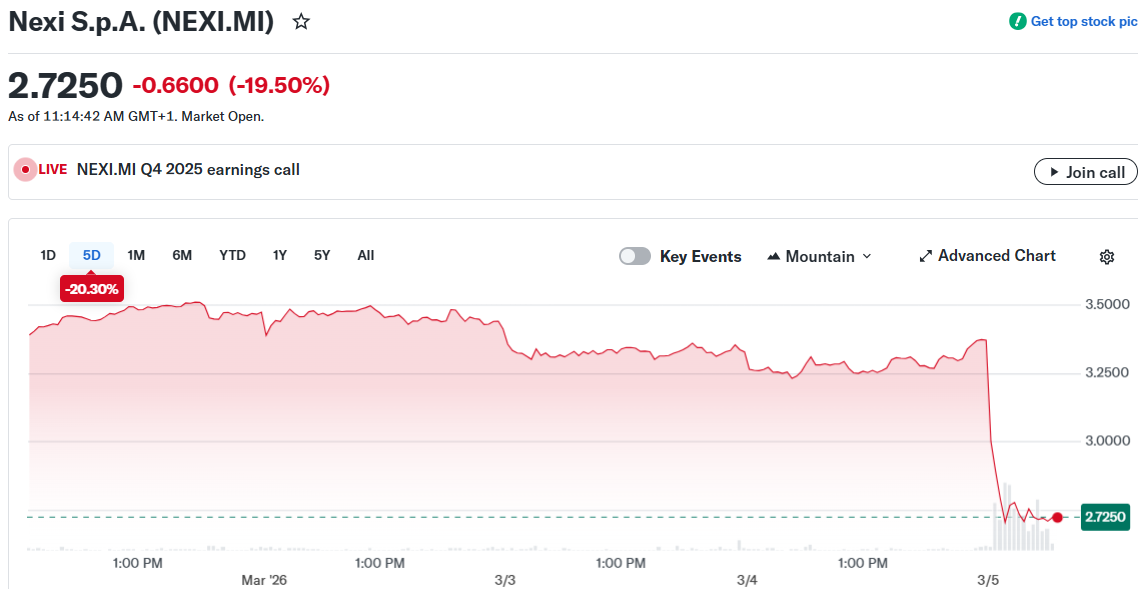

Stock Plunges 20% on Disappointing Q4 Results and Conservative Outlook")

Key Takeaways

- Nexi’s shares plummeted more than 20% to an all-time low following Q4 results that marginally underperformed analyst forecasts.

- The payment processor’s 2026 outlook suggests analysts may need to lower earnings estimates going forward.

- Top-line expansion is projected to stay unchanged in 2026, matching 2025’s modest 2.1% increase.

- Management anticipates generating €2.4 billion in surplus cash flow from 2026 through 2028, with shareholder distributions surpassing €1.1 billion.

- The company’s updated three-year roadmap aims to achieve mid-single-digit revenue expansion by 2028.

Shares of Italian payments processor Nexi experienced a devastating session Thursday, plummeting over 20% to unprecedented lows following the release of fourth-quarter figures that marginally missed projections and a three-year strategic plan that market watchers interpret as foreshadowing downward earnings revisions.

The market reaction was immediate and brutal, although certain industry observers believe the punishment may have been excessive.

Fourth-quarter revenues remained stagnant at €942.5 million, falling approximately 1% short of analyst projections. Adjusted EBITDA declined to €508.6 million, missing consensus forecasts by roughly 2%. Operating expenses increased on a year-over-year basis to €433.9 million.

Performance was hampered by persistent challenges stemming from banking sector merchant portfolio M&A transactions and contract renegotiations. Management indicated these headwinds reached their maximum intensity during Q4 2025, though cautioned they will persist as obstacles throughout 2026 before gradually diminishing.

During an investor presentation in Milan, CEO Paolo Bertoluzzo spoke frankly: “You don’t have to believe we can go to the moon.” He acknowledged that pricing concessions were granted to certain banking partners to retain their business, while noting the company continues to feel the effects of agreements terminated in previous years.

2026 Outlook Remains Subdued

Looking ahead to 2026, Nexi anticipates revenue momentum will mirror 2025’s trajectory, which delivered top-line advancement of 2.1%. The company expects EBITDA to remain approximately flat as it channels resources into strategic growth initiatives.

Morgan Stanley equity analyst Adam Wood characterized the guidance as one that “implies consensus downgrades” across both 2026 and the medium-term horizon. Jefferies described the quarterly performance as “broadly in-line” while highlighting that 2026 projections “may feel more ambitious than at first glance.”

Jefferies researchers also expressed interest in learning more about Nexi’s approach to “ignite growth without risking further contract losses.”

The competitive landscape provides critical context. Technological innovation continues reshaping the payments sector, empowering nimbler competitors to offer more aggressive pricing than established players. Traditional operators such as Nexi, which constructed its market position through acquisitions of bank payment operations, face heightened vulnerability to these competitive dynamics.

Multi-Year Strategy and Capital Allocation

Nexi’s refreshed medium-term blueprint emphasizes targeting mid-market enterprises as a defensive strategy to preserve market position, with full-year revenue advancement expected to reach mid-single digits by 2028. Management also anticipates EBITDA margin improvement by the conclusion of the planning period.

The organization projects approximately €2.4 billion in surplus cash generation spanning 2026–2028, including roughly €750 million during the current year following strategic capital deployment and elevated tax obligations.

Management has put forward a dividend proposal of €0.30 per share, with intentions to increase the distribution by no less than 5% each year throughout the next three years. Aggregate shareholder returns are forecast to surpass €1.1 billion through 2028.

Bertoluzzo characterized the capital return pledge as a mechanism to demonstrate confidence in the underlying business fundamentals during what the organization describes as a “transition year.”

Notwithstanding the dramatic selloff, several analysts observed that the 2025 earnings shortfall was relatively minor and that medium-term projections weren’t substantially different from previous expectations.

According to Nexi’s assessment, Q4 2025 represented the maximum impact from contract renegotiation pressures, with headwinds expected to progressively diminish moving forward.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants