TLDR

Major U.S. equity benchmarks declined sharply as heightened geopolitical risks in the Middle East prompted investors to retreat from riskier holdings.

Crude oil rallied substantially, with Brent briefly surpassing $82 a barrel before moderating later in the trading day.

The Dow Jones, S&P 500, and Nasdaq Composite all posted losses amid worries over inflation and supply chain disruptions.

Defense contractors and energy companies outperformed while airline and technology shares faced selling pressure.

Market participants are closely monitoring inflation trends and the forthcoming employment report for clues on future direction.

Wall Street experienced a broad decline as escalating conflict in the Middle East prompted a risk-off shift among traders, with energy commodities rallying sharply.

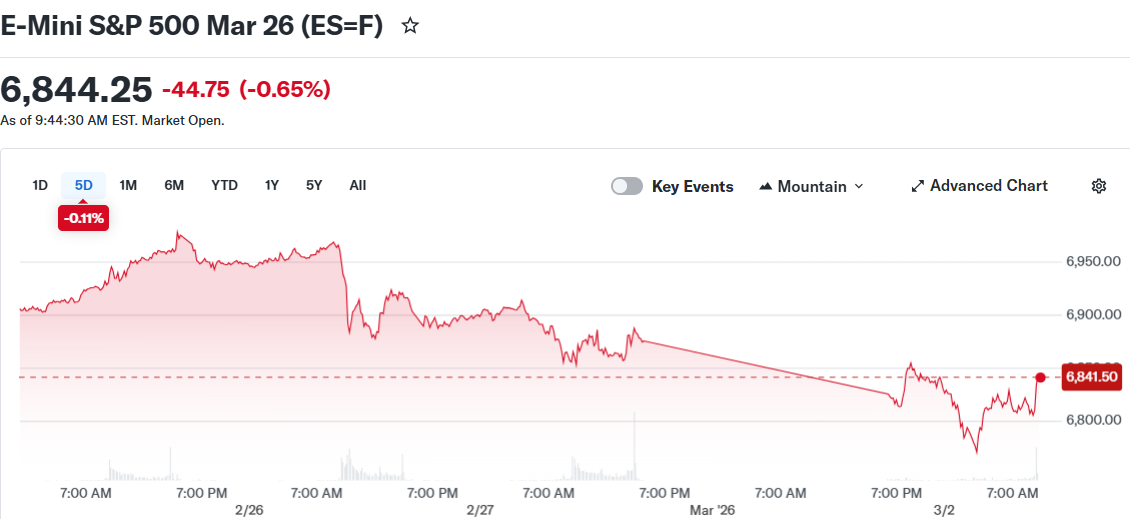

The Dow Jones Industrial Average dropped over 500 points during morning hours. Both the S&P 500 and Nasdaq Composite slid approximately 1% as market turbulence intensified.

The downturn came after military operations involving the United States, Israel, and Iran. Retaliatory actions and warnings regarding critical energy assets heightened market jitters.

Oil prices jumped dramatically as market participants priced in possible supply interruptions. Brent crude spiked as much as 13% to exceed $82 a barrel before retreating toward $80.

West Texas Intermediate also posted significant gains. The benchmark traded around $73 per barrel, representing an approximate 8% advance.

Energy Markets and Inflation Risks

The Strait of Hormuz emerged as a critical concern for petroleum markets. Potential disruptions to shipping traffic through this vital waterway amplified supply worries.

Approximately 20% of worldwide crude production passes through this strategic chokepoint. Reduced vessel movement has intensified expectations of tighter supplies.

Rising energy costs carry implications for inflation dynamics. Market observers are evaluating whether prolonged crude price strength could impact central bank policies.

Treasury yields advanced throughout the trading period. Financial markets scaled back forecasts for imminent Federal Reserve rate reductions.

Gold prices advanced as market participants sought refuge in traditional defensive investments. The U.S. dollar index posted gains versus other major currencies.

Industry Performance and Outlook

Energy sector equities rallied alongside petroleum prices. ExxonMobil posted gains while aerospace and defense firms like Lockheed Martin attracted investor interest.

Transportation stocks faced headwinds. Carriers such as Delta Air Lines retreated on concerns about elevated jet fuel expenses.

Technology shares broadly underperformed. Artificial intelligence and cloud computing names continued experiencing volatility.

Fixed-income securities declined as borrowing costs rose, mirroring inflation anxieties connected to energy price momentum. Portfolio rebalancing occurred across multiple asset categories.

The imminent U.S. employment report has become a focal point for investors. Forecasters anticipate job creation will decelerate from the prior reading.

International financial markets remain highly reactive to Middle Eastern developments. Crude price trajectories and inflation forecasts are driving investor positioning.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants