Key Takeaways

- U.S. equity benchmarks finished last week in positive territory, with the Nasdaq climbing 1.7%

- Financial giants like JPMorgan Chase, Goldman Sachs, and Bank of America deliver quarterly results on Tuesday

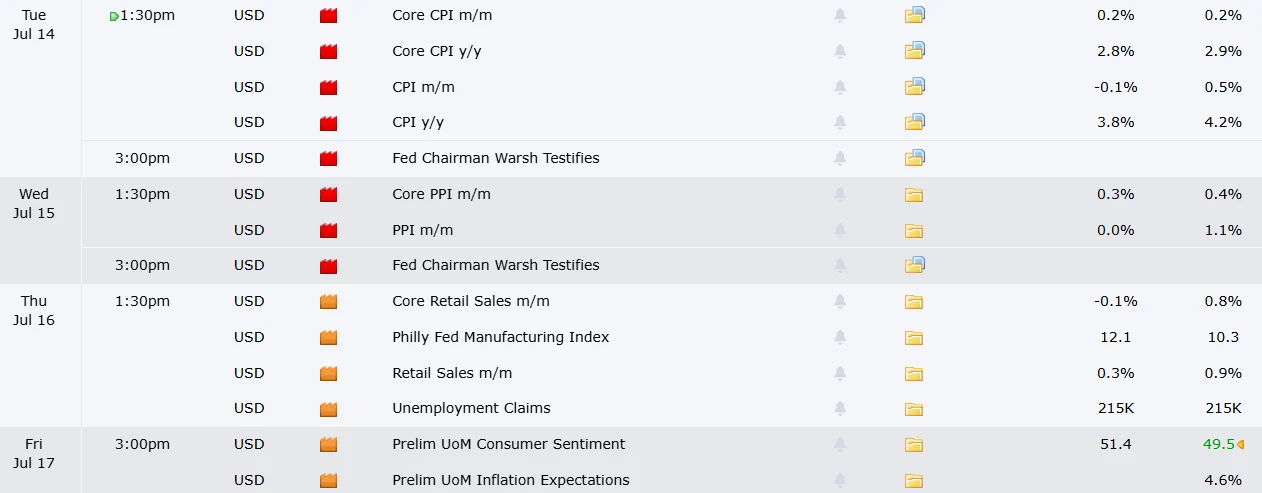

- Consumer Price Index released Tuesday, Producer Price Index Wednesday — forecasts point to modest monthly retreats

- Artificial intelligence equities, especially Nvidia and Micron, projected to fuel 40% of S&P 500 profit expansion

- Federal Reserve maintains data-driven approach while markets anticipate one rate increase before year-end

Financial markets are entering one of their most action-packed periods of the calendar. Second-quarter corporate reporting season launches in earnest, crucial inflation metrics arrive midweek, and traders are scrutinizing whether the artificial intelligence momentum can sustain itself.

The S&P 500 advanced 0.42% on Friday, capping a weekly gain of 1.2%. The Nasdaq posted a 1.7% weekly advance. The Dow underperformed, shedding 0.5% over the five-day period.

Financial Giants Spearhead Corporate Results Season

Tuesday marks a critical milestone. JPMorgan Chase, Goldman Sachs, Bank of America, Wells Fargo, and Citibank deliver their quarterly performance reports simultaneously. Morgan Stanley and BlackRock follow suit on Wednesday.

Financial institutions have benefited from favorable conditions. Initial public offering momentum and elevated trading activity have supported the sector, with market watchers anticipating another robust performance from banking operations.

Wednesday’s calendar includes Johnson & Johnson, United Airlines, and Kinder Morgan. Thursday features Taiwan Semiconductor Manufacturing Company, Netflix, and UnitedHealth.

Expectations remain elevated following an impressive first quarter. LPL Financial chief equity strategist Jeffrey Buchbinder emphasized that margins represent the “key to potentially keeping up this torrid pace of earnings growth.”

He stressed that revenue expansion in the low-teens range must translate into profit growth at least double that velocity. This dynamic places substantial emphasis on artificial intelligence to generate tangible productivity improvements.

Buchbinder highlighted that semiconductor manufacturers Nvidia and Micron by themselves are projected to represent 40% of aggregate S&P 500 earnings expansion. AI infrastructure companies more generally are anticipated to deliver approximately 60%. Beyond technology, only the energy segment is forecast to contribute more than a single point to earnings-per-share advancement.

Critical Inflation Metrics on Deck

Two pivotal price pressure indicators arrive during the week’s middle stretch. The Bureau of Labor Statistics publishes Consumer Price Index figures on Tuesday. Economic forecasters project a 0.1% monthly decline following May’s 0.5% surge.

Producer Price Index statistics arrive Wednesday. Analysts similarly expect a 0.1% month-over-month retreat after May’s substantial 1.1% jump.

Measured annually, headline CPI is anticipated at 3.8% with headline PPI at 6.2%. Both figures would represent deceleration from May’s yearly prints of 4.2% and 6.5% respectively. Core CPI, which excludes volatile food and energy components, is likewise expected to demonstrate slower annual progression.

These statistics carry significant weight as the Federal Reserve continues pursuing its 2% inflation objective. Market pricing reflects one quarter-percentage-point rate increase by the December policy gathering, based on Bloomberg intelligence.

Fed Chair Kevin Warsh has avoided providing explicit forward guidance. Records from June’s Federal Reserve meeting revealed that nearly all committee participants remained open to maintaining current policy or easing if inflation moderates, though nearly all also expressed willingness to tighten if price pressures prove persistent.

Capital.com analyst Daniela Hathorn observed that Warsh’s decision against clear directional signals leaves markets “highly data dependent.”

Friday concludes the week with the University of Michigan consumer sentiment survey, providing additional perspective on American households’ economic outlook.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants