Stock Surges Past Samsung to Claim South Korea’s Top Market Cap Position")

Key Highlights

- SK Hynix eclipsed Samsung Electronics to claim the title of South Korea’s largest publicly traded company by market capitalization, reaching $1.35 trillion

- Shares have skyrocketed over 340% year-to-date, powered by explosive growth in high-bandwidth memory (HBM) chip sales for AI applications

- The company commands 61% of the worldwide HBM market, significantly outpacing Samsung’s 17% and Micron’s 21% market shares

- Samsung, which has maintained the top position for over two decades since 2000, contends that its total market cap including preferred shares stands at approximately 2,252 trillion won

- Reports indicate SK Hynix is considering a Nasdaq listing in the United States to expand its shareholder base

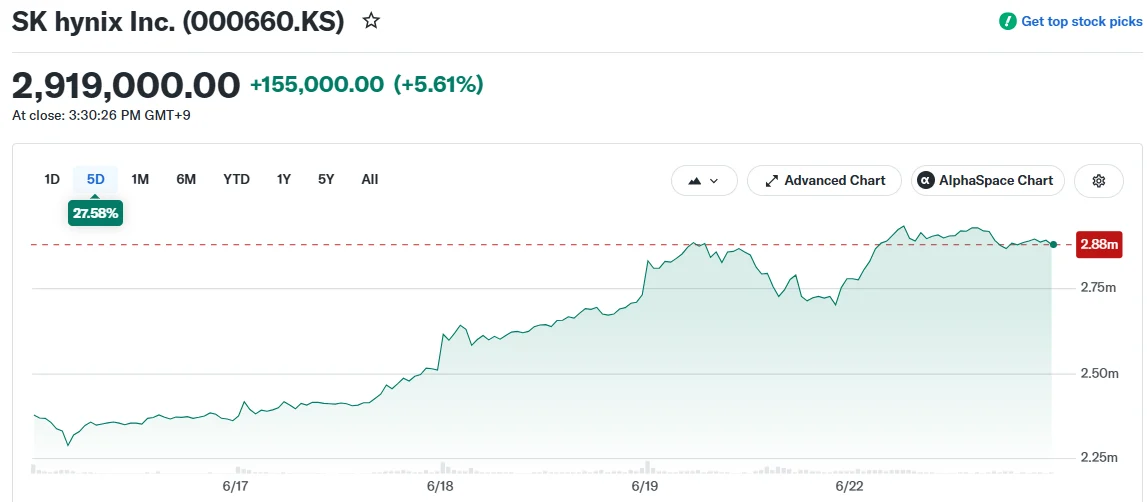

SK Hynix shares climbed 5.7% during Monday’s trading session, elevating its market value to 2,082.5 trillion won ($1.35 trillion) and narrowly surpassing Samsung Electronics — which posted a modest 0.4% gain — marking a historic shift in South Korea’s corporate landscape.

Samsung has occupied the number one position for more than two decades. The margin between the companies remains extremely tight, and Samsung maintains that when preferred shares are factored in, its total market capitalization stands at approximately 2,252 trillion won.

This achievement represents the culmination of an extraordinary year for SK Hynix, with shares climbing more than 340% throughout the period.

The driving force behind this explosive growth is HBM — high-bandwidth memory technology that uses vertical stacking to achieve superior performance and energy efficiency. These specialized chips have become critical components in AI processors manufactured by Nvidia and deployed by tech giants including Alphabet’s Google.

Unlike conventional DRAM chips, HBM is deeply integrated with AI infrastructure. This integration creates substantial competitive moats and provides manufacturers with pricing advantages that commodity memory products could never achieve. SK Hynix commands 61% of the worldwide HBM market. Samsung controls 17%, while Micron holds 21%.

Remarkable Transformation from Near-Bankruptcy to $1.35 Trillion Giant

The company’s resurrection narrative is nothing short of extraordinary. Back in 2002, the company — then operating as Hynix Semiconductor — faced potential acquisition by Micron after drowning in debt. When negotiations collapsed, the firm remained under creditor supervision for almost ten years. By 2003, share prices had plummeted to 135 won — penny stock territory.

In 2023, a severe memory market slump delivered another blow. SK Hynix recorded an annual operating loss totaling 7.73 trillion won during that period.

Despite the challenging environment, the company maintained its HBM investment strategy throughout the downturn — a calculated risk that delivered remarkable returns. In 2024, it achieved record operating profits of 23.5 trillion won as AI infrastructure spending from Microsoft, Google, and Meta intensified.

SK Group Chairman Chey Tae-won, who championed the original Hynix acquisition against significant internal resistance, articulated his strategic vision in a January publication.

“What I really wanted to accomplish when we acquired Hynix was to transform it from a commodity memory producer into a mainstream semiconductor company whose products are indispensable,” he said.

He added: “In the past, it did not matter whether memory came from Hynix, Samsung or Micron. HBM is different. If SK Hynix’s HBM is replaced with another product, the AI system may not function properly.”

Samsung’s Production Advantage Faces Mounting Pressure

The competitive dynamics extend beyond market capitalization metrics. Samsung’s long-standing leadership in DRAM manufacturing capacity is facing increasing challenges.

According to Bank of America projections, SK Hynix’s monthly DRAM production volume will hit approximately 589,000 wafers this year, compared to Samsung’s roughly 691,000. However, SK Hynix is forecast to boost output by 38% from 2025 through 2028, while Samsung’s expansion rate is projected at about 17.5%.

By 2028, these trajectories would reduce the production differential to less than 10%, down from 23% in 2025.

“Previously, the difference in manufacturing scale meant there was simply no way for rivals to close the profitability gap with Samsung,” said Kim Sunwoo, senior analyst at Meritz Securities.

SK Hynix is also reportedly exploring a US listing on the Nasdaq exchange, a move that would significantly enhance its visibility among international institutional investors.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants