TLDR

- The greenback weakened following Trump’s announcement that an Iran peace agreement could be finalized within days

- Crude oil tumbled to eight-week lows amid expectations of reduced tensions and renewed energy supplies

- The euro climbed to weekly highs, poised for its strongest weekly performance in five weeks

- May producer price data in the U.S. exceeded expectations overall, though core metrics fell short of forecasts

- The Fed is anticipated to maintain current rates at next week’s meeting; traders see 60% probability of December tightening

The greenback tumbled Friday following President Donald Trump’s declaration that a peace agreement with Iran could be completed imminently, potentially this weekend. Trump indicated that Iran’s Supreme Leader had approved the framework, diminishing concerns about escalating military tensions across the Middle East.

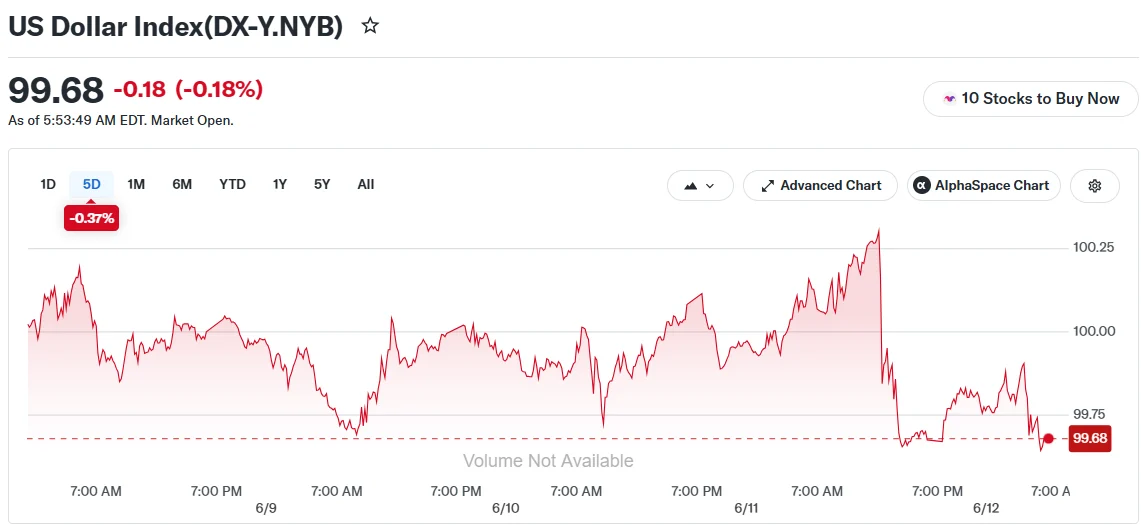

The U.S. Dollar Index declined 0.1% to settle at 99.803 during London trading hours, touching its weakest point in seven days during overnight sessions. The index was trending toward a 0.3% loss for the week.

Whenever market confidence strengthens, the dollar typically weakens. This occurs as traders shift capital away from traditional safe-haven instruments when geopolitical concerns diminish.

“At present, markets are experiencing relief that additional escalation may be prevented, bringing us nearer to a resolution,” noted Mohit Kumar, economist at Jefferies.

Oil prices experienced a significant selloff, plunging to their weakest levels in roughly eight weeks. The decline in crude oil exerted additional downward pressure on the dollar, considering America’s status as a net petroleum exporter.

Euro and Pound Maintain Strength

The euro traded close to its strongest position in seven days and was heading for its most impressive weekly gain in over five weeks. The European Central Bank’s first rate hike in almost three years provided underlying support for the single currency.

Sterling showed minimal movement Friday while maintaining its trajectory for the best weekly showing in nearly four weeks. The British currency shrugged off economic data revealing a 0.1% contraction in the U.K. economy during April, marking the first monthly decline since last August.

The pound’s recent momentum remains tentative. Market participants are closely monitoring the June 18 Makerfield by-election, as outcomes could carry political implications for Prime Minister Keir Starmer.

The Bank of England convenes next week with widespread expectations of maintaining current policy rates. Central bank officials navigate conflicting pressures from persistent inflation alongside decelerating economic growth.

“Elevated prices stemming from Middle Eastern conflict are anticipated to sustain pressure on a vulnerable UK economy,” stated Danni Hewson from AJ Bell.

Fed Under Scrutiny as Inflation Signals Prove Contradictory

U.S. producer price inflation accelerated beyond projections in May, predominantly influenced by elevated energy expenses connected to previous Middle Eastern disruptions. Nevertheless, core producer inflation, excluding volatile food and energy components, registered below anticipated levels.

The conflicting figures alleviated some concerns regarding an imminent Federal Reserve policy tightening move. Market expectations for additional rate increases shifted toward the latter portion of the year.

The Federal Reserve convenes next week with broad consensus anticipating unchanged policy rates. Traders will scrutinize Chair Jerome Powell’s remarks for any indications regarding future monetary policy direction.

Current market pricing reflects approximately 60% probability of a rate increase materializing by December, based on CME FedWatch tool data.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants