Key Takeaways

- SK Hynix is pursuing an American depositary receipt (ADR) offering on US exchanges, potentially raising as much as $14 billion during the latter half of 2026.

- The memory chipmaker reported operating profits of 45 trillion won with an impressive 72% operating margin during the first quarter of 2026.

- Shares have climbed approximately 158% year-to-date, bringing the company’s market capitalization near $948 billion.

- Second-quarter HBM revenue projections reach $7.5 billion, representing an 81% increase compared to January export figures.

- Potential headwinds include ongoing labour disputes with subcontractors, foreign exchange volatility, and the threat of US import tariffs on semiconductor products.

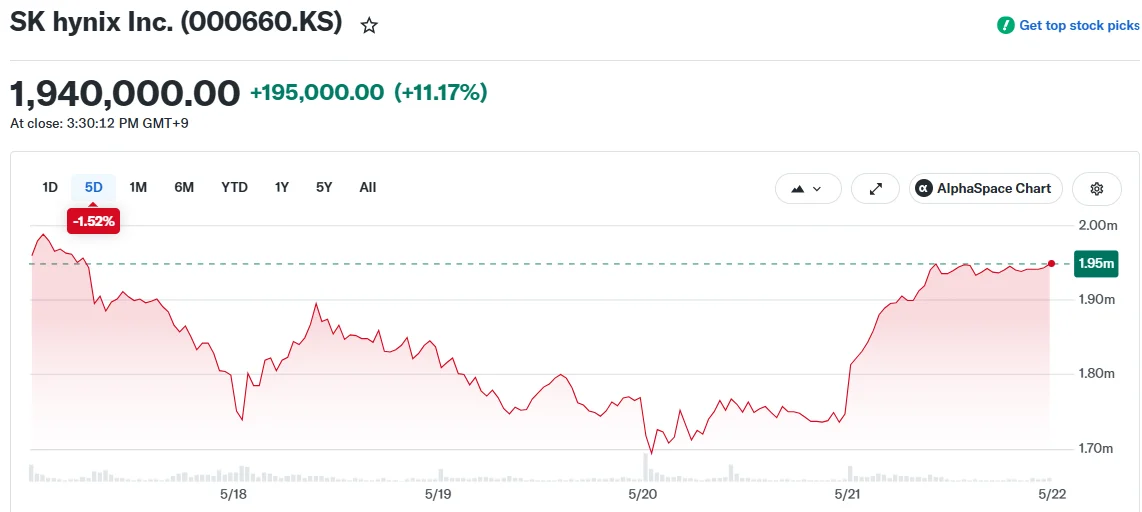

SK Hynix stock experienced an 11% rally during Wednesday’s Korean trading session as anticipation builds around the memory chip manufacturer’s forthcoming American market debut.

The Korean semiconductor giant is moving forward with plans to introduce American depositary receipts (ADRs) on US stock exchanges, with industry sources suggesting a June or July launch window. Media outlets in South Korea indicate the offering could generate up to $14 billion in capital, earmarked for manufacturing facility expansions in both South Korea and Indiana.

This move would provide American retail and institutional investors with direct exposure to a leading AI memory supplier beyond Micron’s dominant position. Until now, Micron Technology has served as the primary vehicle for US-based investors seeking exposure to the high-bandwidth memory (HBM) sector.

Trading at a forward price-to-earnings multiple of approximately 6.1 times versus Micron’s 8.3 times, SK Hynix presents a valuation discount that has attracted attention from investors hunting for opportunities in the AI semiconductor supply chain.

With a current market capitalization hovering around $948 billion, the company is approaching the exclusive trillion-dollar valuation threshold. Share prices have nearly tripled during 2026 alone.

Exceptional Financial Performance Fuels Momentum

First-quarter 2026 revenue reached 52.5763 trillion won, accompanied by a 72% operating margin — metrics that underscore the persistent supply-demand imbalance in the HBM market.

Bernstein research analysts project SK Hynix will deliver approximately $7.5 billion in HBM revenue during the second quarter of 2026, marking a 25% sequential increase. While this estimate falls short of an earlier $8.2 billion forecast, export data from North Chungcheong and Icheon manufacturing hubs revealed an 81% spike from January baseline levels.

Long-duration customer contracts are providing pricing stability that shields HBM products from the cyclical fluctuations common in traditional memory chip markets.

During Dell Technologies World 2026, SK Hynix demonstrated its HBM4 and HBM3E technologies alongside enterprise server memory modules and solid-state drives designed for AI-enabled personal computers, indicating strategic expansion beyond data center applications.

Workforce Tensions and Competitive Dynamics

The company faces challenges on the labour front. A union representing employees at P&S Logis, a logistics subcontractor, is preparing legal measures over compensation disparities between direct SK Hynix staff and contracted workers.

The union intends to leverage the “Yellow Envelope Act,” legislation effective since March that grants subcontractor employees the right to negotiate compensation terms directly with parent corporations.

A potential competitive advantage may emerge from difficulties at rival Samsung Electronics, where an 18-day labour strike is scheduled to commence Thursday. Any production interruptions at Samsung facilities could redirect client orders toward SK Hynix.

SK Hynix previously surpassed Samsung as South Korea’s largest non-financial corporation by market value earlier this year, primarily due to its strategic emphasis on HBM technology development.

Regarding product roadmap developments, initial HBM4E engineering samples are expected in the second half of 2026, with volume manufacturing targeted for 2027.

Specific details regarding ADR offering size and pricing structure remain unconfirmed. Foreign exchange exposure and prospective US import duties on semiconductor products continue to represent considerations for investors monitoring the planned American market entry.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants