Key Highlights

- The U.S. dollar advanced over 1% during the week, marking its largest weekly climb since early March

- Traders now assign a 65%+ probability to a Federal Reserve rate increase by December, compared to less than 20% seven days earlier

- Ongoing U.S.-Iran confrontations maintain elevated crude prices, intensifying inflation concerns

- The British pound dropped to a five-week bottom amid a leadership challenge facing UK Prime Minister Keir Starmer

- The Trump-Xi diplomatic meeting concluded with minimal market movement, though Iran’s blockade of the Strait of Hormuz continues as a focal point

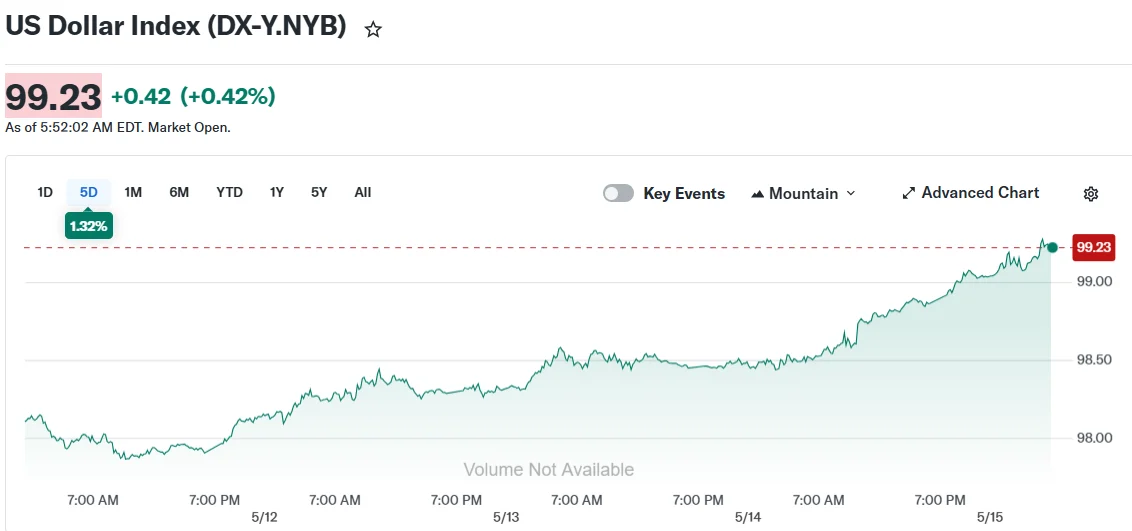

The greenback delivered its most impressive weekly showing in more than eight weeks on Friday, climbing over 1% versus a currency basket to reach a four-week peak of 99.203 on the DXY index.

The advance was fueled by ascending U.S. Treasury yields, which touched annual highs, alongside mounting speculation that the Federal Reserve might implement an interest rate increase before year-end.

Market participants now estimate better than 65% odds of a Fed rate hike arriving by December. Merely seven days prior, this probability stood under 20%, based on CME FedWatch tool data. Trading desks are also fully pricing in a rate adjustment by March 2027.

This dramatic reassessment followed a succession of U.S. economic indicators that exceeded analyst projections. Import price data and wholesale inflation figures both surpassed forecasts during the week’s early sessions. April retail spending demonstrated growth, while weekly unemployment claims signaled labor market resilience.

Continuing friction between Washington and Tehran is compounding inflationary pressures. The Strait of Hormuz blockade persists, maintaining oil prices at elevated levels. Rising energy expenditures are permeating broader inflation metrics, strengthening arguments for Federal Reserve intervention.

“The dollar is catching up with the strong data we’ve seen this week,” said Francesco Pesole, FX strategist at ING. “It feels like there’s a realisation that the U.S. story in an energy crisis may just end up being much better than many other places in the world.”

British Pound Pressured by Domestic Political Turmoil

Sterling descended to a five-week nadir against the dollar, briefly touching $1.3332 before stabilizing slightly at $1.3347. The currency is tracking toward its steepest weekly decline since November 2024.

Prime Minister Keir Starmer confronts an escalating leadership contest following disappointing local election outcomes. Andy Burnham, Greater Manchester Mayor, signaled intentions to pursue a parliamentary position to launch a challenge. Jefferies economist Mohit Kumar observed that investors worry a more progressive leader might expand the UK’s fiscal shortfall.

The euro similarly weakened against the dollar, sliding to a one-month minimum of $1.1632 and positioned to surrender 1.3% across the week.

Trump-Xi Diplomatic Talks Generate Muted Market Response

A forty-eight-hour summit featuring U.S. President Donald Trump and Chinese President Xi Jinping wrapped up Friday. Financial markets demonstrated minimal reaction. Beijing cautioned Washington regarding Taiwan and characterized the U.S.-Iran conflict as something that “should never have started.”

Trump declared his patience with Iran was exhausting and noted both leaders desire the Strait of Hormuz reopening while opposing Iranian nuclear weapons development.

The onshore yuan retreated from a three-year zenith against the dollar to 6.8038, influenced by widespread dollar strength.

Across other Asian markets, the yen depreciated to 158.47 per dollar notwithstanding robust domestic wholesale inflation statistics. The Singapore dollar, Korean won, and Philippine peso similarly drifted lower.

The dollar appreciated 0.3% versus the Malaysian ringgit to 3.945, with Kenanga analysts projecting consolidation between 3.93 and 3.96 throughout the coming week.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants